The $100 Bill Isn’t For You

Did you know that 83% of the value of US currency is in $100 bills?

Over 35% of all physical notes in circulation are hundreds. The next closest denomination is the $1 bill, which accounts for less than 20%. There are more $100 bills in the American economy than any other bill, 19.9 billion of them, holding nearly $2 trillion in value.

I don’t know about you, but I can count on my two hands (okay, that’s generous, my one hand) the number of times I’ve physically held a $100 bill. The average cash purchase in America is $31. Cash makes up just 14% of what we buy. Eighty percent of consumers prefer cards. Most of us carry about $67 in our wallets, and the hundreds that end up there tend to stay there, backup money that sits behind the twenties until we forget about it.

So where are all the $100 bills?

I found out, and the answer is disturbing. A huge share of them aren’t even in the United States. The Federal Reserve estimates that up to half the total value of American currency circulates abroad, much of it held by foreign governments, criminal organizations, drug cartels, and corrupt officials who prize the $100 bill for the same reason you don’t use it: it packs enormous value into a very small, very anonymous package.

There is a solution, and you’re not going to like hearing it. Shred $100 bills. Phase them out. Stop printing them. It would strengthen monetary policy and undercut criminal operations across the globe.

The $100 bill does not benefit our economy.

Where the Money Goes

The foreign demand isn’t all criminal. A 2024 Federal Reserve study by economist Ruth Judson estimated between $750 billion and $1.5 trillion in US currency held overseas. The range is wide because counting cash in foreign mattresses is, predictably, difficult. But much of that demand comes from countries where the local currency can’t be trusted: Argentina, Russia, Ecuador, Vietnam, Cambodia. In places with unstable banks, runaway inflation, or the constant threat of political upheaval, US dollars function as household insurance. Families hold $100 bills because they’re compact, universally recognized, and more stable than anything their own government offers. Not every $100 bill in a foreign safe is dirty money. Some of it is a frightened family’s entire savings.

But the same properties that make the $100 bill useful to a worried family in Buenos Aires make it useful to someone with very different priorities.

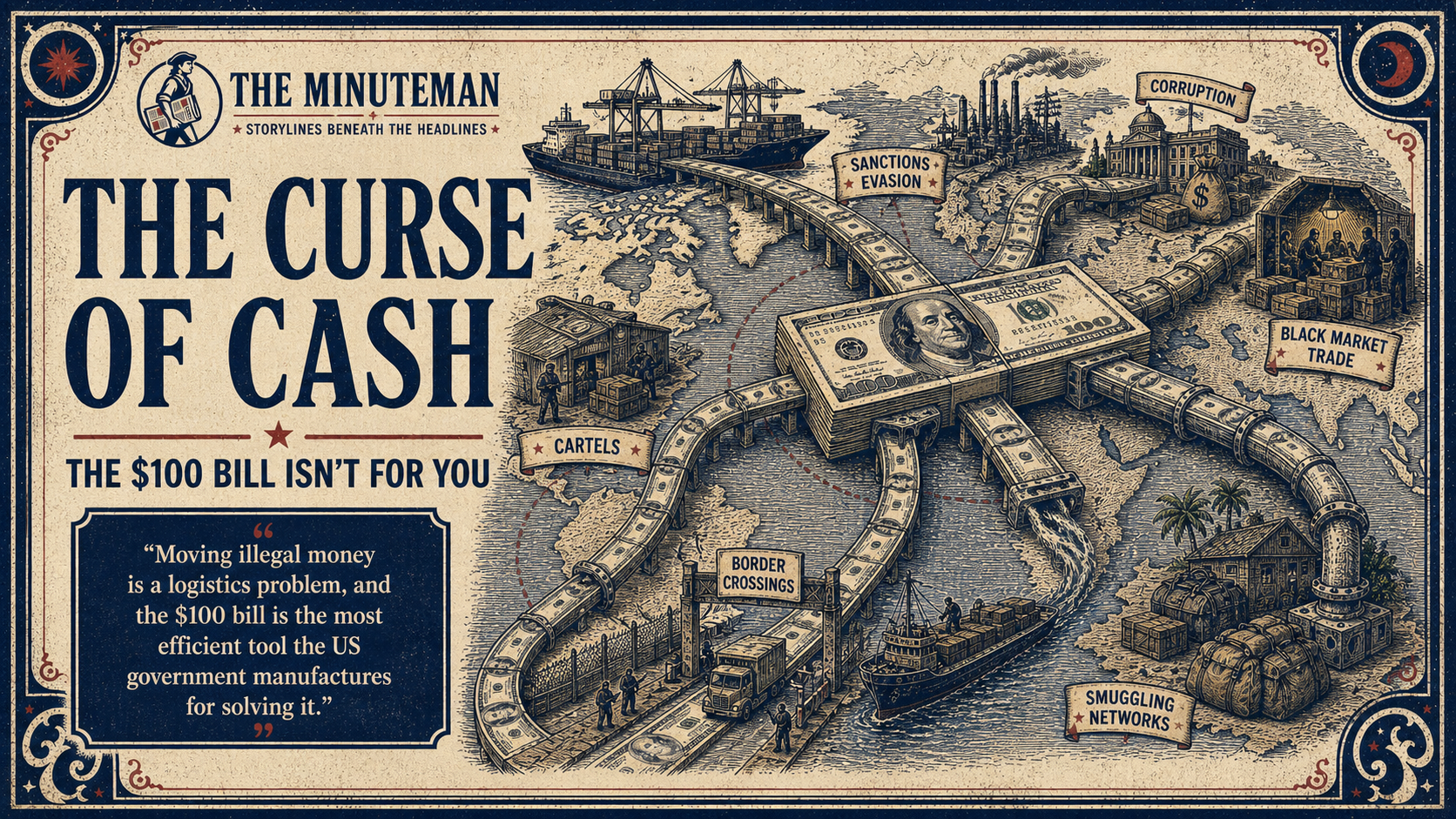

One million dollars in $100 bills weighs 22 pounds and fits in a single briefcase. The same amount in $20 bills weighs 110 pounds and requires four briefcases. The now-discontinued €500 note, which criminals nicknamed “the Bin Laden,” could compress a million dollars into five pounds, a small shoulder bag. Organized crime in Britain paid above face value just to get their hands on €500s. The UK’s Serious Organised Crime Agency reported that 90% of €500 notes sold in the country ended up with criminal organizations.

Moving illegal money is a logistics problem, and the $100 bill is the most efficient tool the US government manufactures for solving it.

In 2007, Mexican authorities seized $207 million in cash from a single home belonging to Zhenli Ye Gon, a pharmaceutical executive tied to methamphetamine precursor trafficking. The hoard was mostly $100 bills. In hundreds, $207 million fits in closets. In twenties, it would have filled a fleet of armored trucks.

The Treasury Department’s 2024 National Money Laundering Risk Assessment confirms what the physics suggest. Dollar banknotes, bulk cash smuggling, and conversion of smaller bills into $100s remain active money-laundering methods. Drug traffickers operating across the US-Mexico border move an estimated $20 to $30 billion in cash annually, running it through “counting houses” that aggregate small street-level bills and convert them to hundreds, quintupling transport efficiency in the process.

The $100 bill serves four major illicit industries. Drug trafficking relies on it for cross-border cash movement. Tax evasion benefits from its anonymity: the IRS estimates the gross tax gap at $696 billion, with $539 billion of that coming from underreporting, concentrated in cash-intensive sectors where transactions leave no automatic record. Self-employed individuals are nearly four times as likely to hold $100 bills as salaried workers, and about 55% of income from sources with little or no third-party reporting goes unreported. Human trafficking and smuggling operations depend on the portability of high-denomination notes to move fees across borders. And terrorist financing, from ISIS oil smuggling operations generating up to $500 million annually to Hezbollah’s laundering networks, requires large-denomination cash to move millions without a digital trail.

None of this means that every $100 bill is criminal. But it means the denomination’s design advantages align less with what ordinary Americans need and more with what illicit economies require.

The Government’s Cut

If the $100 bill creates this much trouble, why does the government keep printing it?

Because the government makes money from the arrangement, and that creates a conflict of interest nobody in Washington is eager to discuss.

The mechanism is called seigniorage, and it works like this: when the Federal Reserve issues paper currency, that currency becomes a non-interest-bearing liability on its books. The Fed holds interest-earning assets against it. The spread between what those assets earn and what the currency costs to produce (a $100 note costs about 11.3 cents to print) generates revenue that historically flows to the US Treasury.

The Fed hasn’t been in a normal remittance environment lately. In 2023 and 2024, higher interest expenses produced net losses rather than the usual stream of payments to Treasury. But the structural incentive hasn’t changed. Nearly $2 trillion in $100 bills circulating worldwide represents an enormous interest-free loan to the American government, provided by whoever is holding those bills, including the cartels, the corrupt officials, and the shadow economies that our own intelligence agencies spend billions trying to combat.

Peter Sands at Harvard Kennedy School calls this “negative development assistance.” Advanced nations earn seigniorage by manufacturing the physical tools for corruption in poorer countries. The issuing state profits from an interest-free loan funded by the tax evaders and criminals who destabilize developing societies. The United States, in other words, prints the instrument, profits from the demand, and then funds agencies to fight the crimes that demand enables.

Why You Can’t Just Stop Printing

So the government profits, criminals benefit, and the $100 bill has outgrown its usefulness to ordinary Americans. The obvious next step is to stop printing them. But that presents a problem.

On November 8, 2016, India declared 86% of its currency illegal overnight. The 500 and 1,000 rupee notes most Indians used for daily life could no longer be spent. The government had printed replacements equal to only about 10% of the voided bills, so three quarters of the country’s usable cash was stranded by morning. People holding the old notes had to deposit them at a bank, wait in long lines, and hope the new bills arrived before they ran out of money. Economic output fell two to three percentage points in the next quarter. The damage hit hardest where workers got paid in cash and small businesses ran on it. And the policy failed its own stated goal: 99% of the withdrawn notes were eventually deposited back at the Reserve Bank of India. The illicit cash the policy was designed to capture returned to the banking system through the front door.

Digital payments did surge. Paytm, India’s largest mobile payment platform, saw traffic increase 435%. But the cost of that digital acceleration was borne almost entirely by the people least equipped to absorb it.

The lesson is not “don’t phase out large bills.” The lesson is “don’t do it like that.” India’s approach was sudden, sweeping, and aimed at most of the cash in a country where cash was everything. An American phaseout should be the opposite: gradual, narrow, and legally clear.

Then we have the privacy concern. Cash allows lawful anonymity. A society with less high-denomination cash could become more surveilled, more dependent on banks and payment processors, more vulnerable to account freezes, outages, and the kind of financial exclusion that hits the poorest people hardest. The Cato Institute argues that cash is a “foundation for freedom” because it permits anonymous transactions outside the reach of both corporations and government. Eliminating large bills, in their view, moves us closer to a surveillance economy.

But does it? Let’s look at a historical response. Larry Summers offered the most useful one: did liberty shrink when the United States stopped printing $1,000 bills in 1969? Is it the government’s obligation to provide every conceivable means of anonymous value storage? Ceasing to print a denomination is not the same as banning cash. The $1, $5, $10, and $20 would all remain. People don’t usually need a $100 bill for groceries or gas or rent. The goal is to remove the denomination whose primary advantage is high-value anonymity while preserving everything else cash does well.

Then there’s the substitution question. If the $100 disappears, criminals will shift to $50s, foreign currencies, gold, crypto, real estate, shell companies, luxury goods. That’s true. Substitution will happen. But forcing traffickers from $100s to $20s quintuples the physical bulk of every shipment. More bulk means higher interdiction rates, more red flags at borders, more friction in every transaction. We don’t reject seatbelts because they don’t prevent every car death. We accept that raising the cost of a dangerous activity is worth doing even when it can’t eliminate the activity entirely.

One more important note: some experts, Peter Sands among them, argue that eliminating the $100 alone isn’t enough if $50 bills remain as the next best alternative. To break the logistics of bulk cash smuggling, the policy should target notes above $50. That’s a harder political sell, but the substitution math supports it.

How to Do It Without Breaking Anything

The model already exists. The European Central Bank stopped issuing €500 notes in 2019 and completed the withdrawal by 2024. Existing notes remain legal tender and can be exchanged at any time, so there was no panic, no demonetization shock, and no sudden losses for anyone holding one.

An American version would follow the same logic. The Federal Reserve and Treasury stop ordering and issuing new $100 bills while continuing to support every smaller denomination. Existing hundreds remain legal tender and fully redeemable, just as the $500, $1,000, $5,000, and $10,000 notes discontinued in 1969 still are today. Banks accept $100 bills from customers but stop recirculating them. Returned notes go to the Fed for destruction and get replaced with smaller denominations. Reporting rules kick in for unusually large bulk redemptions, treating them as risk signals without penalizing ordinary people cashing in a few hundreds from a birthday card (side note: if your grandma is giving you $100s in your birthday card you better treasure that woman).

Then there’s the international dimension. Millions of $100 bills circulate abroad as household savings in countries with fragile currencies. A phaseout needs a diplomatic and foreign-exchange plan that gives foreign holders time and a clear mechanism to convert without losing value.

None of this requires eliminating cash. Smaller bills remain widely available. Nobody needs a bank account, a smartphone, or a credit card to make ordinary payments. The policy removes one denomination from production. The US did this with four denominations in 1969 and the financial system held.

One more thing working in favor of the gradual approach: $100 bills last about 24 years in circulation, compared to 6.6 years for a dollar bill. They last that long because they’re stored, not spent. If the government stops printing new ones, the existing stock shrinks through attrition, giving the economy and foreign holders years to adjust.

The Digital Question

The phaseout conversation usually leads to a digital one: if we reduce high-denomination cash, what fills the gap? Nothing needs to, but the world is moving toward Central Bank Digital Currencies (CBDCs) anyway – we looked at this last week with cryptocurrency (that’s its own problem).

CBDCs aim to replicate what cash does well, instant settlement, accessibility, universal acceptance, while adding traceability. Some newer designs, including research from ETH Zurich, propose digital currency systems that work offline using QR codes or NFC tags, verified by merchants during emergencies and settled once networks return. In theory, this solves one of cash’s most important roles: working when nothing else does.

In practice, CBDCs aren’t ready. China’s digital yuan, the most advanced attempt, accounts for just 0.2% of total digital payment volume after years of development. CBDCs were originally designed to behave like cash, which meant they would earn no interest. In 2026, China broke from that principle and began paying interest on digital yuan balances, an admission that consumers weren’t adopting it voluntarily. The IMF’s 2025 policy paper flagged the same readiness problem from the institutional side: central banks were never built to operate consumer technology, the systems they’re attempting lean heavily on private vendors, and the cybersecurity exposure is a serious concern.

And then there’s the surveillance problem that makes the privacy argument from earlier look quaint. The same traceability that catches criminals can monitor dissidents, freeze accounts on political grounds, and track every purchase a citizen makes. A government with full CBDC adoption has a tool for financial control that would make the authors of the Patriot Act jealous.

Neither CBDCs nor crypto (whose most enthusiastic customers, as I covered recently, tend to be arms dealers, dictators, and at least one sitting president) are ready to replace what cash does well. The emerging reality is probably hybrid coexistence: physical cash for privacy and resilience, digital systems for convenience and traceability. But phasing out the $100 bill doesn’t require a digital replacement. It just requires keeping smaller bills in circulation. The digital question is separate from the denomination question, and pretending it’s been answered would be dishonest.

What Currency Is Supposed to Do

Here is what we know. Eighty-three percent of US currency value sits in $100 bills. Ordinary Americans account for a vanishing share of that demand. The bills circulate through foreign shadow economies, drug supply chains, tax evasion schemes, and laundering networks that the US government simultaneously profits from and spends billions trying to dismantle. We’ve phased out larger denominations before. Other countries have phased out their equivalents. The policy tools exist, the precedents exist, and the evidence is clear enough to act on.

Currency is supposed to do a simple thing: facilitate exchange between citizens. The $100 bill facilitates exchange between cartels, corrupt officials, and a Treasury that earns revenue on every bill outstanding. The most common bill in America isn’t serving America. It’s serving everyone except the people whose trust it was supposed to represent.

In 1969, the government looked at the $500, the $1,000, the $5,000, and the $10,000 and decided the line was $100. Maybe the line needs to move. Not because we need a cashless society, and not because we trust digital alternatives to do what cash does. But because the question at the center of currency has always been the same one: who is the financial system designed to serve?

We already know who the $100 bill serves. The question is whether we’re comfortable with the answer.