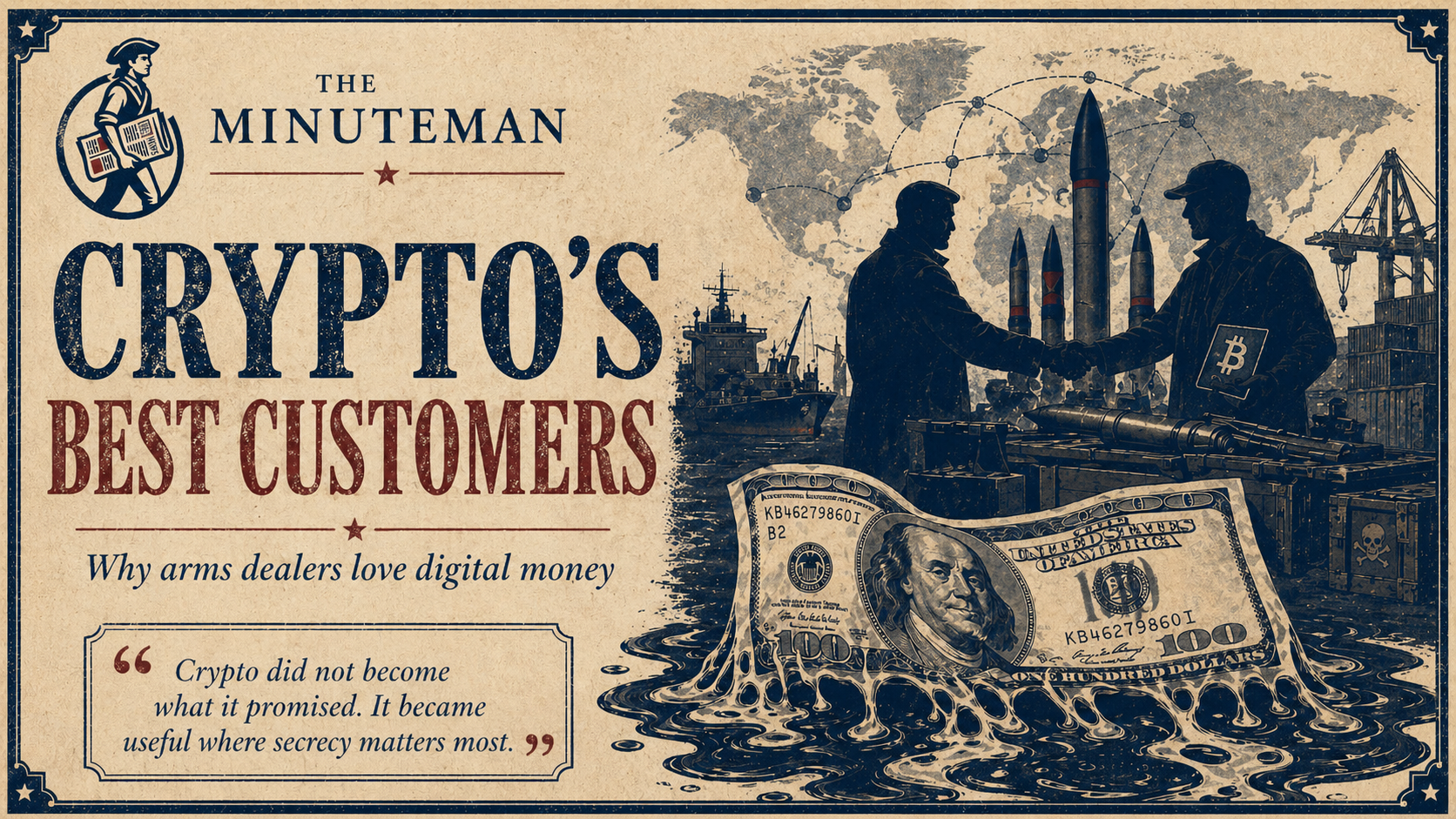

Crypto’s Best Customers Are Arms Dealers, Dictators, and a Sitting President

How a technology built on a lie funds nuclear weapons, pushes us closer to war, and operates exactly as designed.

Who Is This Actually For?

There is a good chance you have a crypto app on your phone right now.

Maybe you downloaded Coinbase during the pandemic because a coworker told you Bitcoin was going to hit a hundred thousand dollars. Maybe you moved some savings into a neobank because the interface was better and the fees were lower and the old bank charged you twenty dollars a month just for having an account. Maybe you bought fifty dollars of Ethereum because someone on a podcast said decentralized finance was the future and you did not want to be the person who missed it.

Or maybe you did none of that. Maybe you just keep hearing about it. The Super Bowl ads. The arena sponsorships. The coworker. The brother-in-law at Thanksgiving who will not stop talking about blockchain. You have been told, repeatedly and from every direction, that cryptocurrency is the future of money, that you are early, that the financial system is about to change and you should get in before it does.

You have also been told, in the same breath, that cryptocurrency is a scam, a bubble, a casino dressed up in the language of liberation.

Both of those things contain truth, and neither of them is the full picture.

The full picture is worse than either side is telling you, and it is worse in ways that do not require you to own a single coin to affect your life. Because the central feature of cryptocurrency is not the technology. It is the ability to move money without attaching a name to it. Transactions are recorded on a public ledger, but the people behind them are not. That is not a flaw in the design. It is the design. And when you build a financial system where money moves in the dark, the people who benefit most are not the ones in the Super Bowl commercials. They are the ones who need money to move where no one is looking.

North Korea’s military hacking unit has stolen $6.75 billion in cryptocurrency and used the proceeds to fund its nuclear weapons and ballistic missile programs. Iran, locked out of the international banking system, is using crypto to sell armed drones and ballistic missiles, fund militia networks, and, according to Bloomberg, charge ships up to $2 million each to pass through the Strait of Hormuz. Russia legalized cryptocurrency for international settlements the same year it needed to evade sanctions over its invasion of Ukraine. Across all sanctioned jurisdictions, $15.8 billion in crypto flowed to sanctioned entities in 2024, with Russia and Iran as the primary recipients. In total, $154 billion in cryptocurrency moved to illicit addresses in 2025, a 162 percent increase from the year before.

This is not a story about an app on your phone. This is a story about what happens when accountability is removed from a financial system and the worst people in the room are the first to notice. And whether you own a single coin or not, you are already inside it, because the political system that is supposed to protect you from this is being purchased by the people who profit from it.

Crypto with Chad and Brad

Before we go any further, we need to answer a question that turns out to be harder than it should be.

What is cryptocurrency?

If you have asked this question to someone who owns crypto, you have probably received one of several answers, none of which left you feeling like you actually understood the thing. You might have heard the word “blockchain.” You might have been told it is “digital money” or “decentralized finance” or “the future of the internet.” You might have been told that you just don’t get it yet, and that is exactly what they said about the internet in 1995.

The fact that cryptocurrency is hard to explain is not a sign that it is complex. It is a sign that clarity is not in the seller’s interest.

So here it is in one sentence. Cryptocurrency is a digital token, created and tracked by a network of computers, that people buy, sell, and trade on the belief that it will be worth more later than it is now.

That is it. There is no building behind it, no factory producing goods, no government backing it, no revenue stream, no dividends, no earnings report. There is a token, and there is a price, and the price moves based on how many people want to buy it versus how many people want to sell it.

The technology underneath is called a blockchain, which is a record of every transaction that has ever occurred on the network. Think of it as a giant public notebook. Every time someone sends crypto to someone else, that transaction is recorded in the notebook, and the notebook is stored on thousands of computers around the world so that no single person controls it. The people who run those computers and verify those transactions are called miners, and they are rewarded with new tokens for the work. This is how new cryptocurrency enters the system.

The promise is that because no single bank, government, or company runs the notebook, no one can manipulate it. The system is supposed to be “decentralized,” meaning no one is in charge.

That is the theory. Now let’s watch it happen.

Chad is twenty-six and works in tech. He started hearing about Bitcoin from a podcast he likes, then from a coworker, then from about forty different accounts on social media. He downloads Coinbase, puts in $500, and buys some Bitcoin. He does not fully understand what he bought, but he understands that the price has been going up, and he understands that the people telling him to buy it seem confident.

The price goes up ten percent. Chad is thrilled. He tells his friend Brad about it. Brad puts in $500 too. Now there are two buyers. The increased demand pushes the price up a little more. Chad’s original $500 is now worth more than he paid for it, not because Bitcoin produced anything or generated revenue, but because Brad bought some.

Chad and Brad tell their friends. A few of them buy in. The price goes up again. Chad is now sitting on a profit, and he has never been more certain that this is the future of money. He has also never tried to buy groceries with Bitcoin, because almost no one does. Seventy-six percent of all crypto transaction volume is derivatives trading, which is a technical way of saying people are betting on the price going up or down. The overwhelming majority of crypto activity is speculation, not commerce.

But Chad doesn’t think about that. Chad thinks about the number on his screen going up.

Now imagine the new friends stop buying. No new money enters the system. The price flattens. Some of the friends who bought late get nervous and sell, which pushes the price down. Brad is now sitting on a loss. Chad, who got in earlier, is still up, but only because Brad and the others bought after him. The only way Chad makes money is if someone else buys his tokens at a higher price than he paid. The only way that new buyer makes money is if someone after them does the same thing.

Now zoom out. Imagine an asset that does not produce anything. It does not pay interest or dividends. It is not used to buy groceries or pay rent in any practical volume. Its price goes up when more people buy it, and it goes up faster the more people who have heard of it. The people who got in earliest make the most money. The only way those early people cash out is if people who got in later buy from them at a higher price. It is promoted, in practice, disproportionately to young men (the crypto industry spent $3.5 billion on marketing in 2025 alone, much of it targeted at exactly this demographic). The people telling them to buy on social media already own the asset and benefit when others buy it. When somebody questions whether it has any actual value, the standard answer is that if you had gotten in earlier you would not be asking.

What is another word for that?

Some might call it a Ponzi scheme, an arrangement where early participants are paid with money contributed by later participants, and the scheme only holds up as long as the flow of new money keeps growing. Economists have another. They call it the greater fool theory, an investment whose return does not depend on the thing being worth anything but on finding somebody willing to pay more than you did. A third term is pyramid scheme, which is the retail version of the same structure.

The crypto community will object to all three, and they have points worth addressing. A traditional Ponzi scheme has a central operator who promises returns and pockets the money. Bitcoin has no central operator. The structure is different. The strongest version of the counter-argument is that Bitcoin functions like digital gold: a scarce asset that holds value over time, independent of any government’s monetary policy. Gold does not pay dividends either. Gold does not generate revenue. People buy gold because they believe other people will continue to value it, and that belief has held for thousands of years. If Bitcoin can establish the same kind of trust, the argument goes, then the lack of cash flow is not a flaw. It is the point.

That argument isn’t total B.S., and for some investors it has worked. Bitcoin has made people money. But gold has six thousand years of demonstrated stability, an industrial use case in electronics and jewelry, and a physical reality that does not depend on an internet connection or a private key you can lose. Bitcoin has existed for seventeen years, has lost more than fifty percent of its value in a single year on multiple occasions, and functions in practice less as a stable store of value than as a speculative vehicle that swings wildly on sentiment and social media momentum. The comparison to gold is aspirational, not descriptive.

And the people who study this for a living keep arriving at the same conclusion. Nassim Nicholas Taleb, the mathematician and author of The Black Swan, has called Bitcoin an “open Ponzi scheme.” Warren Buffett has described crypto holders as engaged in a “greater fool” game. An academic chapter published in a major finance series titled it without hedging: “Bitcoin: Worse Than a Ponzi.” In August 2024, the SEC charged a company called NovaTech with running a $650 million fraud that blended multi-level marketing with cryptocurrency, paying early investors with money from new recruits until the whole structure collapsed.

The structural differences between Bitcoin and a classic Ponzi scheme are real. But the economic result for the average participant is the same. Early holders profit. New entrants absorb the losses. The pitch is always “you’re early.” And the people doing the pitching already own what they are selling you.

El Salvador tried to prove the skeptics wrong. In 2021, the government made Bitcoin legal tender, the first country in the world to do so. Citizens were required to accept it. Four years later, ninety-two percent of the population had not used Bitcoin for daily transactions. The government reversed course. Bitcoin acceptance was made voluntary in 2025 as part of a deal with the International Monetary Fund.

An entire country tried to make crypto work as money. It did not work as money.

The anger that built the machine

If cryptocurrency is this flawed, the question is why it exists at all. And the answer is that the anger that created it was real.

In 2008, the global financial system collapsed. Banks that were supposed to safeguard the economy had instead gambled it into ruin, packaging bad mortgages into complex financial instruments, selling them to investors, and collecting massive fees along the way. When the bets went bad, the losses were catastrophic. The U.S. government bailed out the banks with public money. Millions of Americans lost their homes anyway.

On January 3, 2009, someone using the name Satoshi Nakamoto created the first block of the Bitcoin blockchain. Embedded in that block’s code was a headline from The Times of London: “Chancellor on brink of second bailout for banks.” It was a timestamp and a thesis. The banks had failed. The government had rescued them with your money. Nakamoto proposed a system that required neither.

No bank. No government. No middleman. A currency that belonged to no one and could not be manipulated by the powerful few who had just burned the house down. Power to the people.

That was the pitch. And if you have ever waited on hold with your bank, or been charged a fee for having too little money in your account, or watched the institutions that crashed the economy receive bonuses the following year while your neighbors lost their houses, you felt the pull of that pitch. Most people did.

But before we decide whether crypto delivered on that promise, we need to look clearly at the thing it was supposed to replace.

The U.S. dollar is also just something we decided has value. That sounds strange, but it is true. The dollar has not been backed by gold since 1971, when Richard Nixon ended the gold standard. Before that, every dollar in circulation was theoretically redeemable for a fixed amount of gold held in federal reserves. After that, the dollar was backed by the “full faith and credit” of the United States government, which is a formal way of saying: we all agreed this piece of paper is worth something, and the agreement holds because the government says it does and because everyone else agrees too.

This is not a flaw. This is how all modern currency works. The euro, the yen, the pound, every major currency on the planet operates on the same principle. We assign value, and the system functions because there are institutions, laws, and accountability structures that maintain the agreement. If a bank commits fraud, regulators can pull its license. If a currency is mismanaged, elected officials answer for it. If the system breaks, there are mechanisms, imperfect and sometimes painfully slow, for holding the people who broke it accountable.

Crypto proposed something different. Not just a new kind of money, but a new philosophy of money. What if we removed the institutions entirely? What if no one was in charge? What if the system ran on code instead of trust?

The problem is that trust was not the disease. Trust was the immune system. Flawed, inconsistent, sometimes failing in spectacular fashion, but still the only mechanism that allows you to hold someone accountable when things go wrong.

When you remove trust from a financial system and call it a feature, the question becomes: what happens when that system breaks, and who answers for it?

The answer, as it turns out, is no one. And that answer has consequences.

The people’s currency and the people’s share of it

The standard way economists measure wealth inequality is a tool called the Gini coefficient. A score of zero means everyone has the same amount. A score of one means a single person has everything. The traditional global wealth system, all the fiat currencies and real estate and stock markets combined, sits at roughly 0.8. That number is bad. It means about twenty percent of the people hold about eighty percent of the wealth.

Bitcoin’s Gini coefficient, depending on the methodology and how you cluster wallet addresses, ranges from roughly 0.65 to as high as 0.98. One blockchain analysis from Elementus pegged it at 0.842. The currency of the people is more concentrated than the system it was supposed to replace.

When Chad bought crypto on Coinbase, he thought he owned crypto. He didn’t. Coinbase holds it for him in their wallet, the same way a bank holds cash in a vault. He does not have a private key. He does not control the wallet. If Coinbase freezes his account, gets hacked, or goes bankrupt, his Bitcoin may be inaccessible, locked, or lost entirely. And he has no FDIC insurance, no deposit protection, and no recourse outside of whatever Coinbase decides to do about it. FTX proved exactly this. Customers thought they owned crypto, and then one morning they didn’t. Chad traded one intermediary for another. Except this one has no license on the wall.

A fair objection: wallet addresses are not the same as people. Coinbase holds a single cold wallet on behalf of millions of customers. When that mega-wallet shows up in the data as “one address,” the raw concentration numbers get inflated. Analysts have argued that once you adjust for exchange custody and identifiable entities, the ownership picture improves.

It improves. It does not equalize.

Even after adjusting for custodial accounts, the top ninety-four non-exchange wallets each hold more than ten thousand Bitcoin, worth over a billion dollars apiece at current prices. MicroStrategy, a single company, holds 762,099 Bitcoin. BlackRock’s iShares Bitcoin Trust holds 785,852. The wallets holding less than one full Bitcoin, the ones the crypto community calls “shrimp” (which tells you something about how the hierarchy is internalized), collectively own a fraction of the total supply that barely registers on a chart.

The people at the bottom of this system named themselves after something small and disposable, and nobody at the top corrected them.

In the early days, anyone could mine Bitcoin on a laptop. The network was designed to be distributed. But as the asset became valuable, the economics of mining changed. The hardware evolved from household computers to specialized machines that cost tens of thousands of dollars. Mining operations migrated to regions with the cheapest industrial electricity. The people with the most capital built the biggest data centers, mined the most Bitcoin, and swallowed the network.

Today, two mining pools, Foundry USA and AntPool, control approximately sixty percent of Bitcoin’s total computational power. If those two entities agreed to coordinate, they could theoretically alter or censor the transactions on a network whose entire value proposition is that no one can alter or censor the transactions.

And the exchanges are not much better. Coinbase stores ninety-eight percent of customer crypto in cold storage and retains fifteen to thirty-five percent of staking rewards. Robinhood holds $51 billion in crypto assets under custody. These are not scrappy alternatives to Wall Street. These are financial institutions, functioning identically to the banks crypto was supposed to replace, except without FDIC insurance, without deposit regulation, and without the capital requirements that traditional banks are forced to maintain.

You have not escaped the middleman. You have traded a regulated middleman for an unregulated one. The concentration of wealth is the same or worse. The corporate control is the same or worse. And the protections you had, thin as they were, are gone.

So if this system is not decentralized, and it is not equal, and it is not building an alternative to institutional finance, the question becomes: what is all that centralized, unaccountable power actually being used for?

What anonymity buys

The first major commercial use of Bitcoin was the Silk Road, an online marketplace that operated on the dark web from 2011 to 2013. It facilitated the sale of illegal drugs, forged documents, and other contraband, processing 9.5 million Bitcoin in transactions before the FBI shut it down. Its founder, Ross Ulbricht, was convicted and sentenced to two life terms in prison. President Trump granted him a full and unconditional pardon on January 21, 2025.

The Silk Road was not an aberration. It was a proof of concept. Crypto’s core feature, the ability to move money without revealing who you are, turns out to be the most valuable product in criminal finance. (Shocker.)

In 2025, darknet markets processed $2.6 billion in cryptocurrency. Roughly 3.2 million users access these platforms through encrypted browsers. That is the retail level: individual people buying drugs, stolen data, and forged identities with digital tokens that cannot be easily traced back to them.

Jeffrey Epstein understood the utility early. In 2015, Epstein provided $850,000 to MIT’s Digital Currency Initiative, invested $3 million in Coinbase during its Series C round, and put another $500,000 into Blockstream, a Bitcoin infrastructure company. Developers who received funding through the MIT initiative have stated they were unaware of Epstein’s involvement and that his money carried no conditions affecting their technical work. There is no evidence he steered Bitcoin’s development. But what do you think he was so interested in Bitcoin for? Epstein’s primary operations were trafficking, blackmail, and money laundering, all of which require moving money in ways that cannot be traced. Paying victims, buying silence, receiving blackmail payments, laundering the proceeds. A financial system designed so that no one can see where the money goes is not a curiosity to someone running that kind of operation. It is the infrastructure.

But individual crime, even at Epstein’s scale, is the small end of what anonymity enables.

Iran has been locked out of the SWIFT international banking system since 2012. For years, that exclusion was one of the most powerful tools the United States had to pressure the regime without military action. Financial sanctions are not a bureaucratic abstraction. They are the primary mechanism the United States uses to project power short of sending soldiers to die. When sanctions work, they constrain hostile governments by cutting off their access to the global financial system. Wars that might have been fought are instead resolved, or at least contained, through economic pressure.

Cryptocurrency is drilling a hole through that wall.

Iranian wallets received $7.8 billion in crypto in 2025. The IRGC, Iran’s military and intelligence apparatus, received over $3 billion in crypto in 2025, accounting for more than half of all Iranian crypto activity by the final quarter. Those funds went to militia networks, dual-use military equipment, and oil sales. In late 2024, Iran’s Defense Export Center began accepting cryptocurrency for military hardware: armed drones, ballistic missiles, naval vessels. By March 2026, the regime was charging ships up to $2 million each to transit the Strait of Hormuz, payable in Bitcoin.

Russia followed a parallel path. After its invasion of Ukraine triggered sweeping sanctions, crypto became a primary tool for evasion. The Duma legalized cryptocurrency for international settlements in July 2024. Putin announced the legalization of crypto mining the following month. More than a hundred no-KYC exchanges now operate in Russia, allowing users to transfer funds from sanctioned banks and receive crypto without verifying their identity.

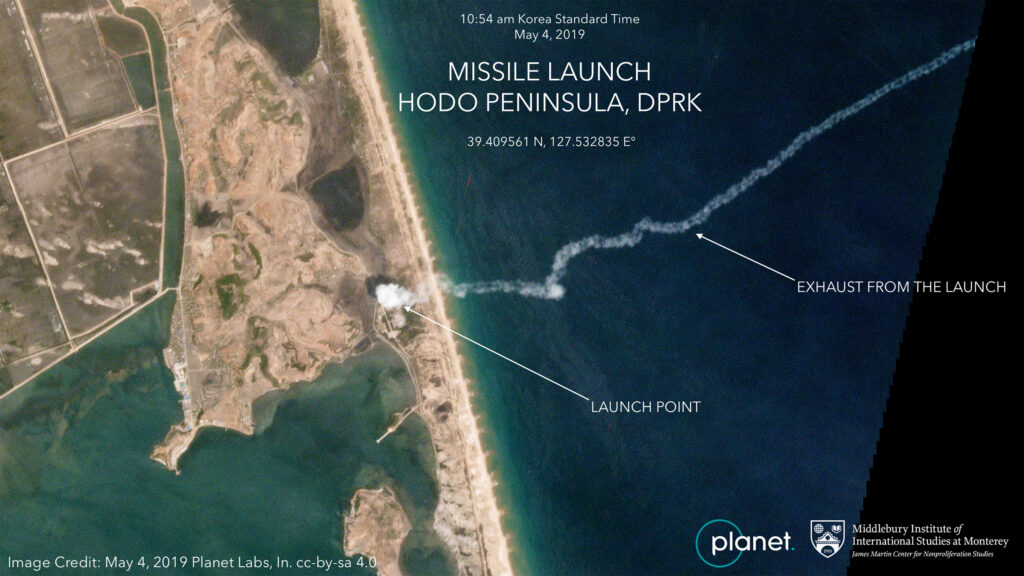

And then there is North Korea. The Lazarus Group, the regime’s military hacking unit, stole $2.02 billion in cryptocurrency in 2025. The $1.5 billion Bybit heist was the largest single theft in the history of cryptocurrency. North Korean operatives created fake identities, applied for remote jobs at Western crypto startups, worked as employees for months learning internal systems, then drained the treasuries. An investigation found nearly one hundred alleged North Korean engineers embedded inside more than fifty Web3 projects. The cumulative total stolen by the regime across roughly 270 documented incidents sits at an estimated $6.75 billion. U.S. officials have estimated that about half of the regime’s missile program is funded through these operations, though the precise breakdown of funding sources remains classified.

The pattern is the same at every scale. An individual buying drugs on the dark web and a nation-state funding a nuclear weapons program are using the same feature of the same technology for the same reason: no one can see who they are.

When sanctions lose their teeth, the menu of options shrinks. Diplomacy without economic leverage is diplomacy without consequences. What remains is confrontation, and confrontation means people dying in ways that financial pressure was specifically designed to prevent. Every dollar that moves through an anonymous crypto wallet and into the hands of a sanctioned regime is a dollar that weakens the alternative to war.

Cryptocurrency’s advocates describe anonymity as a right. For the people funding missiles, it is a business model.

The quarter-billion-dollar campaign to keep it this way

If everything you just read is true, the natural question is: why isn’t the government doing something about it?

The answer is that the people profiting from the system are spending unprecedented amounts of money to make sure no one writes the rules.

In the 2024 election cycle, crypto corporations poured between $119 million and $245 million into federal elections, depending on how you count affiliated spending. By the narrower measure, that $119 million in direct corporate contributions represented forty-four percent of all corporate money in the entire election. Not forty-four percent of tech money. Forty-four percent of all corporate money, from every industry combined. The crypto super PAC Fairshake, funded primarily by Coinbase, Ripple, and Andreessen Horowitz, raised $202.9 million and spent it electing pro-crypto candidates at a ninety-one percent success rate across fifty-eight targeted races.

The spending was not abstract. It had specific targets.

Senator Sherrod Brown of Ohio was the chairman of the Senate Banking Committee and one of the most prominent voices calling for crypto regulation. Fairshake spent $40 million backing his Republican opponent, Bernie Moreno. Moreno won. The chairman of the committee most responsible for regulating crypto was removed from office by crypto money.

In California, Fairshake spent $10 million opposing Katie Porter’s Senate bid. Porter’s crime was not a legislative record on crypto. She was an ally of Elizabeth Warren, whom the industry considers its primary opponent. Porter lost her primary.

Representative Jamaal Bowman of New York received $2 million in Fairshake spending against him. Representative Cori Bush of Missouri received $1 million. Representative Al Green of Texas, a longtime crypto critic, faced $1.5 million from Fairshake’s affiliate PAC in 2026 and was given an “F” rating by Stand with Crypto, a Coinbase-backed scorecard, based largely on a single statement referring to his opponent’s backers as “MAGA-backed crypto bros.”

For the 2026 midterms, the industry has committed $288 million. The previous record for corporate group spending in a midterm election was $18 million, by the National Association of Realtors in 2022. Crypto is outspending that record by a factor of sixteen.

The effect is visible across party lines. Under Biden, Democrats were broadly skeptical of the crypto industry. Within a year of this spending, over a hundred House Democrats were voting for crypto-friendly legislation that would exempt parts of the industry from the same financial oversight applied to banks and brokerages. The shift did not happen because the evidence changed. It happened because the money changed.

There is an irony at the center of this. The entire philosophy of cryptocurrency is decentralization. No one in charge. No concentration of power. And the industry built on that philosophy has become one of the most aggressive, centralized political forces in the country, using the money it made from “decentralization” to purchase centralized power over the legislative process.

And nowhere is this more visible than at the top.

The Trump family launched World Liberty Financial, a crypto venture whose token and associated products have generated at least $1.4 billion in revenue over sixteen months, with billions more in unsold tokens. The president’s $TRUMP memecoin, launched on January 17, 2025, surged to a $27 billion market cap within a day. It has since fallen ninety-six percent. Fifty-eight wallets made millions. Seven hundred sixty-four thousand wallets lost money. The token’s code automatically routes a cut of every transaction to wallets tied to the project’s creators, meaning the Trump-affiliated entities continue profiting from trading activity regardless of the price collapse. More than $324 million in fees have flowed to those wallets.

Meanwhile, the Trump administration dropped or froze eighty-nine cryptocurrency enforcement cases, dismissed SEC lawsuits against Coinbase and Kraken without penalty, and disbanded the Justice Department unit responsible for crypto crime regulation. A top DOJ official who shut down enforcement against crypto companies held more than $150,000 in personal crypto investments.

Senators Elizabeth Warren and Jack Reed raised concerns that World Liberty Financial may have sold tokens to buyers linked to North Korean hackers, Russian sanctions evasion networks, and Iranian exchanges. They called for a national security investigation. The company disputed some of the specific claims, and some turned out to be false alarms. But WLF also confirmed it had rejected millions of dollars from purchasers who failed its compliance screening. If the filters caught millions in suspect money trying to get in, the question is not whether the filters worked. The question is who was trying to buy in.

A sitting president is profiting directly from the same unregulated system his administration is responsible for regulating, while that system is being used by the adversaries his government claims to be confronting. This is not an opinion. It is a sequence of events that anyone can verify.

What Brad and Chad think

At this point in the article, the crypto bros are probably ready to burn me at the stake. You have either read this far because you agree or you are holding an objection and waiting for it to be addressed. Or, in the case of Brad and Chad, you are waiting for me to print my address across the bottom of the article so you can come and take up your objections with me in person. (Please don’t.) There are a lot of different arguments people use when they argue for cryptocurrency, but let’s talk about the main ones.

The technology is useful, even if the currency is not. This is true, in a narrow and specific way. The cryptography underneath a blockchain is not particularly advanced. Public-key cryptography, the method that lets you sign and verify a transaction without revealing your identity, dates from the 1970s. What Bitcoin introduced was the removal of the trusted intermediary: the bank, the clearinghouse, the institution that sits between you and the person you are paying. In theory, removing the middleman is elegant. In practice, the middleman being removed is a licensed, regulated institution with consumer-protection obligations, and removing it is not an upgrade. It is the opposite of one. There are legitimate uses for distributed ledger technology, mostly in cross-border settlement and supply-chain tracking, and those applications have been quietly built by banks and logistics firms without using Bitcoin or any cryptocurrency at all. The utility is real. It is also small. The industry has sold the public on it being neither.

Crypto is a hedge against inflation. The daily volatility of Bitcoin, measured against gold or the dollar, has for most of its history been roughly four to five times higher than either. A hedge is something that reduces risk. Something that can lose half its value in a week is not a hedge. It is a risk. What Bitcoin has been, over certain long windows, is an asset that has appreciated. That is a different thing. And it has appreciated because more people have bought it. (So did Beanie Babies).

You are just mad you did not get in early. So is everyone that got involved in a Ponzi scheme. Do you think everyone who “invested” with Bernie Madoff is upset they didn’t get in earlier? The early investors with Bernie Madoff made money too (at first). Nobody would look at them and say the problem with Madoff’s critics is that they were jealous they did not get in sooner. If a structure’s stability depends on newer participants paying older participants, and the older participants’ response to criticism is that the critics should have joined earlier, the argument has quietly admitted what it is. It is not a defense of the system. It is a description of the system. And it matches, almost word for word, the SEC’s working definition of a Ponzi scheme.

The banking system is broken too. Yes. It is. The American financial system is unfair in specific, measurable, documented ways. Black and Latino borrowers pay higher rates for the same risk profile. Overdraft fees extracted twelve billion dollars from low-balance accounts in 2024 alone. Consumer protection structures are weaker than they should be. That is a real problem. It is also the argument for fixing the system, not for replacing it with one that has no protections at all. A broken accountability structure can be rebuilt. A system designed to have no accountability structure cannot be made accountable without rebuilding it from scratch.

Crypto cannot be banned anyway. Correct. Nobody serious is arguing that it should be (that ship has sailed). The European Union has not banned crypto. Japan has not banned it. Singapore has not banned it. The argument I am making is not about prohibition. It is about whether the instruments that make sanctions evasion, nuclear procurement, and political capture possible will be permitted to continue operating without a regulatory floor. That question has been answered in other countries. It has not been answered here.

An important caveat: the crypto industry is not a monolith. There are developers building on blockchain technology who genuinely want regulation. Smaller exchanges have lobbied for licensing standards that would weed out fraud and separate legitimate operations from criminal ones. Compliance-oriented companies have spent years asking for clear rules so they can build businesses without waiting to see if the federal government decides to sue them. The internal fight over what crypto should become is real and ongoing. But the people winning that fight are not the developers asking for clarity. The people winning that fight are the ones writing the checks, and the checks are buying a version of the future that serves the checkwriters.

So what do we do?

The situation is not hopeless. Other countries have already started doing what the United States has not.

The European Union passed a comprehensive crypto regulation that went into full effect in December 2024. It requires crypto companies to obtain licenses, verify who their customers are, maintain reserves, and disclose risks to buyers. In its first months, crypto scam reports dropped fifty-eight percent compared to the same period the year before, and regulators forced hundreds of unregistered crypto firms to shut down. The United Kingdom, Singapore, and Japan have built similar frameworks, all applying the same basic principle: if you handle people’s money, you follow the same rules whether you operate out of a bank branch or a blockchain.

These are not hostile-to-crypto jurisdictions. They are countries that decided clear rules protect everyone, including legitimate businesses that want to operate without being confused with criminals.

The United States, meanwhile, has passed almost nothing. The only major crypto legislation signed into law covers one narrow corner of the market and explicitly exempts it from the same oversight applied to banks and brokerages. Broader regulation has stalled in the Senate. If it does not advance before Congress shifts to campaign mode this summer, the country defaults to what it has been doing for years: no rulebook, just lawsuits.

The single thing the crypto industry fears most is disclosure. Real regulation would require crypto projects to reveal who runs them, how they make money, what risks they carry, and where the money goes. Anonymous founders would have to identify themselves. Projects with no revenue model would have to say so. The concentration of tokens in insiders’ hands would be public information. The reason the industry has spent $288 million on midterm elections is not because it opposes all regulation. It is because it opposes the kind of regulation that would require it to tell you the truth.

There are two things you can do about that.

The first is vote, but the vote only works if you know what you are voting for. Check who is funding the candidates on your ballot. OpenSecrets.org publishes donor records for every federal race. Stand with Crypto, the Coinbase-backed scorecard at standwithcrypto.org, rates politicians on their crypto positions; from their perspective, an “A” means the candidate supports the industry, so read those grades with the full context of what you have just learned. Ask whether the candidate who promises to represent you has already been purchased by an industry that spent more on the last election than every other corporate sector combined.

The second is simpler. You do not have to participate. Remember the structure from earlier: the only way the system works is if new money keeps arriving. Early holders profit when new buyers show up. The price only goes up if someone else buys after you. The entire machine requires recruitment. It requires your money. It requires you. Not participating is not passive. It is a refusal to be the fuel.

The crypto industry has spent enormous resources convincing people that this is about innovation, financial freedom, and the future of money. It is about money and freedom, but not yours. It is about the freedom of oligarchs, arms dealers, sanctioned nations, and a sitting president to move money without anyone watching. It is sold to regular people as “avoid those pesky banking fees” so that it looks like a consumer product instead of what it is: infrastructure for crime at global scale.

It serves the people who need to move money without anyone watching. It serves the early holders who profit when new buyers arrive. It serves the corporations that took a decentralized philosophy and used it to build centralized political machines. It serves the arms dealers, the sanctioned regimes, the intelligence operatives who embed themselves inside startup companies and drain the treasury. It serves a president who profits from the product he is supposed to regulate while his administration dismantles the agencies that investigate crypto crime.

It does not serve Chad and Brad. And it does not serve you.

The system that crypto was built to replace is broken. The banks failed. The bailouts were real. The anger was justified. But the answer to a broken system is not a system with no accountability at all. Cryptocurrency is the same broken system without a license, without oversight, without the ability to pull the plug when things go wrong, and with a wealth concentration that makes the traditional banking system look egalitarian by comparison. The choice between a flawed system with accountability and a flawed system without it is not a difficult one.

None of this is hypothetical. North Korea already has the money, the politicians are already purchased, the enforcement agencies are already disbanded. The danger isn’t coming. It’s here and it’s operating exactly as designed.