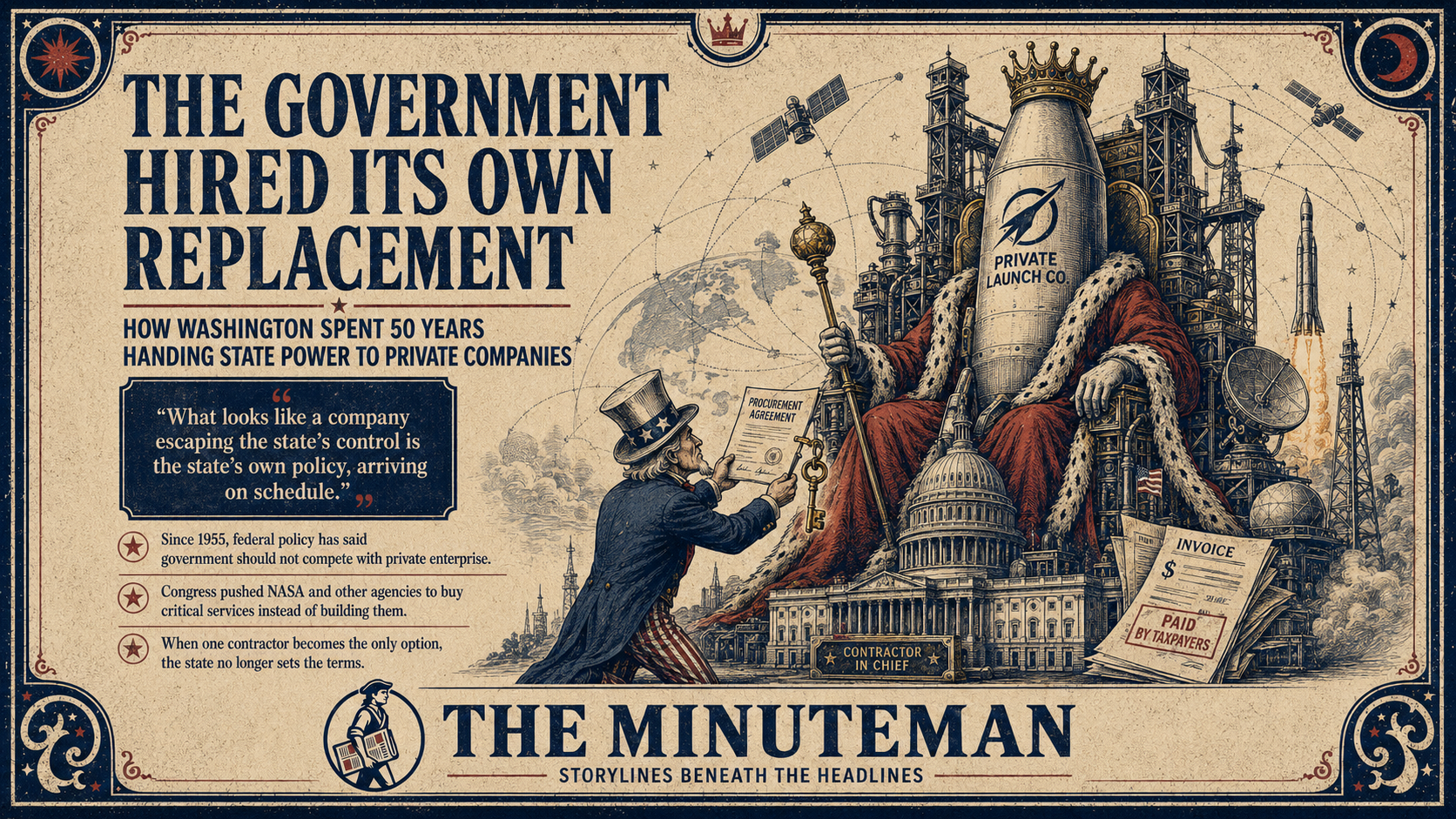

The Government Hired Its Own Replacement

Government privatization didn’t happen to the state — the state chose it, in writing, over fifty years. Now it can’t say no to the companies it created.

In September 2022, a group of Ukrainian drone boats packed with explosives set out across the Black Sea toward the Russian fleet anchored at Sevastopol. As they neared the harbor, the Starlink coverage they needed to complete the run was never there. Ukraine had asked the company to switch on service in the waters off Sevastopol for the strike; the request was refused, and the attack failed.

The person who made that call was not a general, a president, or a defense secretary. He was a private citizen who owned the satellites and had decided the strike was too dangerous to permit. Agreeing to Ukraine’s request, Musk said later, would have made his company “explicitly complicit in a major act of war.”

Set the man aside and look at the arrangement.

One company held a working veto over a battlefield in a war the United States was funding. The easy word for this is capture: a government outmaneuvered by a firm that grew too rich to regulate, the usual traffic of lobbyists and revolving doors and campaign money. That version has the virtue of a villain and the comfort of casting the state as the party that got taken.

It also runs the sequence backward.

The dependency here was not seized from the government. It was handed over by the government, on purpose, in public, in writing, across fifty years, with both parties holding the pen.

The United States helped build the modern launch economy, the internet, and satellite navigation, then wrote policies that moved critical layers of each into private hands.

It still owns and operates some of what it built, GPS above all, but the ability to fly rockets, carry the traffic, and put astronauts in orbit now belongs mostly to companies. What looks like a company escaping the state’s control is the state’s own policy.

There is a rulebook for this, and it is not a metaphor (if you read my stuff enough you’ll learn I love a good metaphor, often to a fault).

Official federal policy, first written down in the 1950s and still on the books, holds that “the Government should not compete” with its own citizens. The Bureau of the Budget began the program in 1955, instructing agencies not to produce for themselves any good or service that private enterprise could supply. Every handoff that follows grows from that single sentence.

So the question, the concern, isn’t about big corporations stealing what used to belong to a government by the people for the people. It is what happens to that government that spends half a century contracting out its own capabilities, and how do you know when the whole thing is going to come crumbling down.

How a state loses faith in itself

The handoff needed a reason before it needed a law, and the reason was a loss of confidence that ran deeper than any single administration.

In the 1970s the American faith in government broke. Vietnam ended the assumption that the state told the truth. Watergate ended the assumption that it obeyed its own rules. Stagflation ended the assumption that its economists understood the machine they were steering, because the reigning theory said inflation and unemployment could not climb together, and then they did.

The institution lost faith in itself first, which is why the retreat that followed was bipartisan. It was not one party’s project. It was a shared conclusion that the government was the problem.

Two economists supplied the intellectual scaffolding.

Milton Friedman argued that markets punish failure the instant it happens while government insulates itself from the consequences of its own mistakes. James Buchanan turned the same skepticism into a discipline, studying the state as self-interested actors rather than selfless public servants, “politics without romance.”

Their case gave privatization something it had lacked: a respectable rationale. Handing a function to the market was no longer a retreat from duty. It was good governance.

Ideology explains why the retreat was permissible. The budget explains why it happened.

As the Cold War wound down, the money that had built the American state’s technical capacity drained away. NASA is the cleanest gauge. At the height of Apollo in the 1960s the agency consumed more than 4 percent of all federal spending. Today it runs near a third of one percent.

As the deficits climbed, a government that could no longer afford to own what it had invented found itself holding a philosophy that told it ownership was a mistake anyway.

The ideology supplied the justification. The deficit supplied the motive. Together they produced a decision that no one ever quite announced: stop building, start buying.

The receipts

An assertion that the government did this on purpose is only as good as the paper behind it, and the paper is extensive. The retreat was legislated line by line, on record, by both parties.

The framework was the Office of Management and Budget’s Circular A-76, the document that carries the “should not compete” language and set up a process for testing whether commercial-type work an agency was doing for itself should instead be opened to private bidders. (That’s the boring stuff, don’t worry we’re done with it.)

In space, Congress wrote the Commercial Space Launch Act of 1984 to license and encourage a private launch industry that did not yet exist. Six years later the Launch Services Purchase Act of 1990 went further and inverted the default, directing NASA to buy launches from commercial providers and reducing the building of its own rockets to a narrow exception. The agency that put men on the Moon was now instructed, by statute, to become a customer.

The same pattern ran through every technology the government had midwifed.

The internet began as a federal network; in 1995 the National Science Foundation decommissioned the NSFNET backbone and turned the wires over to private carriers.

The Global Positioning System, a military program that civilians had been allowed to use for years, delivered only a deliberately degraded public signal until 2000, when the government switched off that degradation and turned precise navigation into a free public utility that private firms could build empires on.

To take stock of what else might be moved out, Congress passed the Federal Activities Inventory Reform Act of 1998, which required every agency to catalog its own commercial-type activities so they could be reviewed for possible outsourcing. The state took an inventory of itself and flagged the parts a private bidder might do instead.

None of this was hidden. It was the announced, celebrated policy of a country that had decided its own hands were the wrong ones for the work.

It worked

The uncomfortable part, for anyone hoping this is a simple story about a mistake, is that the strategy succeeded. The privatizers were right about efficiency, and the numbers are not close.

The Space Shuttle cost roughly 1.6 billion dollars a flight, about 30,000 dollars for every pound it lifted to orbit. A Falcon 9 lists near 67 million, and its first stage flies home and launches again. On cost per pound the private rocket is more than an order of magnitude cheaper than the Shuttle.

The handoff did exactly what it promised. It made access to space cheap.

This is what most people who argue for the privatization of government services lean on during an argument. And they’re right. The market delivered.

The relevant question was never whether privatization would produce a better rocket. It did. The question is what a country loses when the better rocket belongs to someone else.

The hollowing

What it loses is the ability to say no.

When the Shuttle retired in 2011, the United States had no way to put its own astronauts in orbit and would not have one for nine years. In the interval it bought seats from Russia, paying more than 90 million dollars for a single ride by the end. The capability came back in 2020, aboard a SpaceX capsule. It came back belonging to a company.

That is the moment the relationship inverted.

A government that buys a service it can no longer perform is not a customer in any ordinary sense. When there is a line of vendors, the buyer sets the terms. When there is one vendor and no substitute, the vendor does.

The Crimea veto was the inversion made visible: the supplier deciding what the client’s ally could and could not do in a war. Around the same time it happened again in a register no one could miss, when SpaceX wrote to the Pentagon that it could no longer fund Starlink in Ukraine for free and asked the Defense Department to cover a bill approaching 400 million dollars a year.

A private firm had come to invoice the United States for a war. When you are the only applicant, the interview runs the other way.

The exit that was never there

Defenders of the handoff have an answer to all of this, and it is the strongest thing they can say. If a contractor abuses its position, the market corrects it. A supplier that gouges or defies its customer invites a competitor, and the threat of that competitor disciplines the incumbent. Dependence on one firm is a temporary condition, not a permanent one, because the door is always open.

The answer holds only where the door is real, and here it is an illusion painted on the wall.

Market discipline requires a market, which means a second place the buyer can actually go. Look for that place and it is not there.

Amazon has spent years and billions on Project Kuiper and remains far behind schedule; with the company projecting it would fall well short of its July 2026 interim deployment milestone, the FCC granted conditional relief in June.

NASA has kept a government-directed launch program in the Space Launch System, but built for a different job, deep-space human exploration; it costs around 4 billion dollars a flight and has been judged unaffordable by its own auditors, a measure of how expensive government-directed capacity has become even where Washington chose to keep it.

Boeing built a crew capsule to compete with SpaceX and in 2024 left two astronauts on the space station when the vehicle proved too risky to fly them home; they waited nine months and came back on a SpaceX Dragon.

The competitors exist on paper. But not one of them can do the job when the job is due.

This is the flaw the handoff theory rested on and never tested.

Capacity is not a switch that can be flipped back on. Once the engineers scatter, the factories close, and the institutional memory retires, rebuilding costs far more than keeping would have, and takes years the emergency does not grant. The market can discipline a supplier only while the country retains the option of walking away. Walk far enough, for long enough, and the option is gone. What remains is dependence with the illusion of choice.

Britain did this first

The state has started to notice, and its remedy is the tell. In the past two years the government has taken a roughly 10 percent stake in Intel, an equity position in the rare-earth miner MP Materials that made the Pentagon its largest shareholder, and a golden share in U.S. Steel that lets a president veto the company’s biggest decisions.

After fifty years of shedding ownership, the United States is buying pieces of its industrial base back. The instinct is sound. The execution reveals the trap.

When the Space Force set out to build a resilient, secure military data network in orbit, meant to harden the country’s most sensitive communications, the contract to build its backbone, worth 2.29 billion dollars, went to SpaceX.

The push for resilience deepened the reliance on the single company it most needed insurance against.

A government that once did this itself, and now cannot, ends up managing its dependence instead of ending it. That is a specific historical position, and it has been occupied before.

The East India Company was a private firm that came to run a subcontinent, with its own army, its own revenue, and its own foreign policy, while the British state watched and took its cut. By 1773 the company was insolvent, its Bengal lands mismanaged and its finances brought to a crisis that had it demanding a government loan. Parliament faced the choice every state faces when a company it depends on begins to fail. It did not seize the company or let it collapse. It extended financial support, passed the Regulating Act, and asserted parliamentary supervision over a firm it could no longer afford to treat as merely private. It was, in Britannica’s phrase, the first government intervention in the company’s affairs and the beginning of a takeover that would not conclude for another eighty-five years.

That belongs to the same family of state responses as a golden share and a bailout contract: a state reaching for partial control of a private power it can neither replace nor do without. Britain reached for it in 1773. We are reaching for it now.

What time it is

The value of the parallel is that it puts a clock on the present.

The British takeover of the East India Company was not one act but a long sequence, with two bookends separated by a lifetime.

In 1773 came the rescue and the first major assertion of parliamentary control, the government stepping in to steady a firm it could not afford to lose. Full transfer of the company’s governing powers did not arrive until 1858, and it took a catastrophe to force it.

The Indian Rebellion of 1857, a violent collapse of the company’s authority that no one could ignore, finally moved Parliament to pass the Government of India Act of 1858 and transfer the company’s powers and territories to the crown.

The lesson of the eighty-five years between is not that shed sovereignty never comes back. It is that it comes back only after a public failure large enough to force the choice, and it costs far more to reclaim in 1858 than it would have to keep in 1773.

By that clock we are living in 1773, not 1857. The bailout-and-buy-in phase, the golden shares and the equity stakes and the bigger contract with the same firm. The catastrophic public failure that ends the arrangement has not arrived.

The Crimea veto and the Starlink terminals that emergency crews leaned on during the Los Angeles fires were warnings delivered at no charge, one foreign and one domestic, previews of what a genuine failure would look like. The next one will not be free.

There is a new pressure this timeline did not have, and it points the same direction.

In June 2026, SpaceX went public in the largest offering in history, at a valuation approaching 1.77 trillion dollars, and made Elon Musk the first trillionaire on record. A large share of the offering was steered to ordinary investors, and SpaceX has already entered major indexes, pushing the company into the index funds and retirement portfolios of the citizens whose government depends on it.

Britain’s East India Company had the same feature at its height, its stock spread through the portfolios of the members of Parliament who were supposed to check it. A country becomes slow to reclaim a power its own savings are invested in. The dependence acquires shareholders, and the shareholders acquire a reason to look away.

Return to the drone boats stalled off Sevastopol for want of coverage, because they read different now.

That was not a story about one unpredictable man, and not a scandal about a company that got away with something. It was the design working as written, a wartime capability the government leaned on but did not own, exercised at the discretion of its owner exactly as the arrangement always allowed.

The comfort of the capture story is that it implies a fix: catch the company, close the loopholes, take the power back. The harder truth is that there is no loophole to close, because nothing was broken. The rules were written to produce this, by us, over fifty years, on purpose.

Which is also the reason it is not fixed in place. What one Congress wrote, another can rewrite.

The functions were handed away by statute and by circular, and statutes and circulars can be reversed. The country can decide which capabilities it refuses to depend on anyone else for, and pay to keep them, the way it is already paying to buy back steel and chips and rare earths.

That choice is still open, and it is cheaper today than it will be after the failure that forces it. We know what year it is. The only question left is whether we would rather act like it is 1773, while acting is still an option, or wait for our 1857.